30 April 2026 | Jakarta, Indonesia

PT Global Digital Niaga Tbk (the “Company”; IDX: BELI), a pioneer and leading omnichannel commerce and lifestyle ecosystem in Indonesia focusing on serving digitally connected retail and institutions consumers, today announced its first quarter earnings results for the year 2026.

KEY HIGHLIGHTS

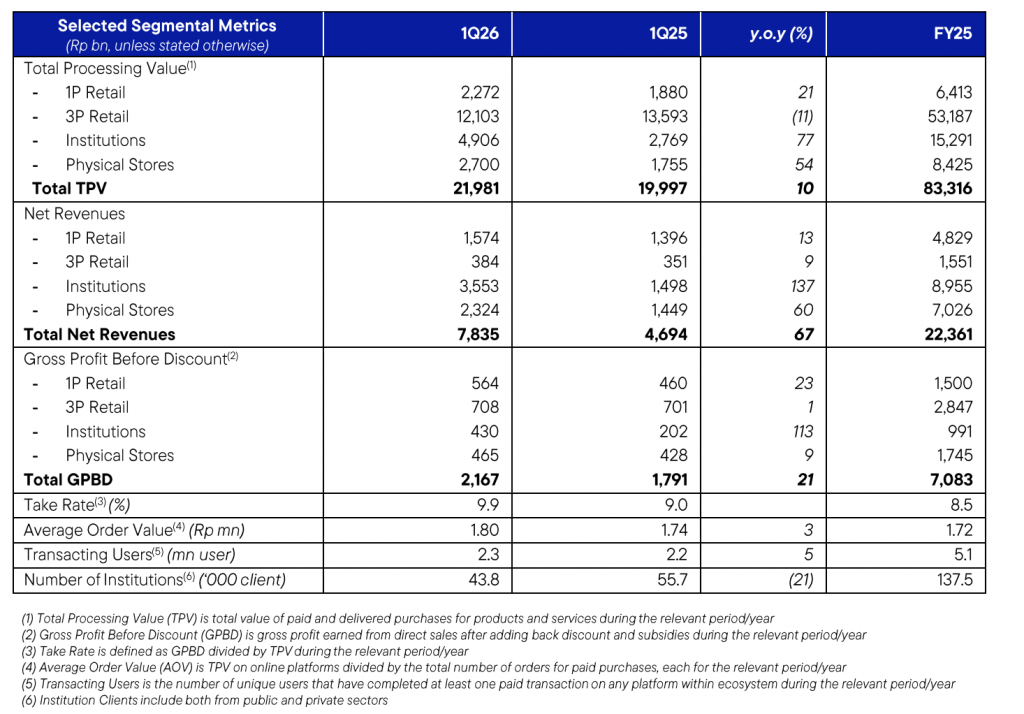

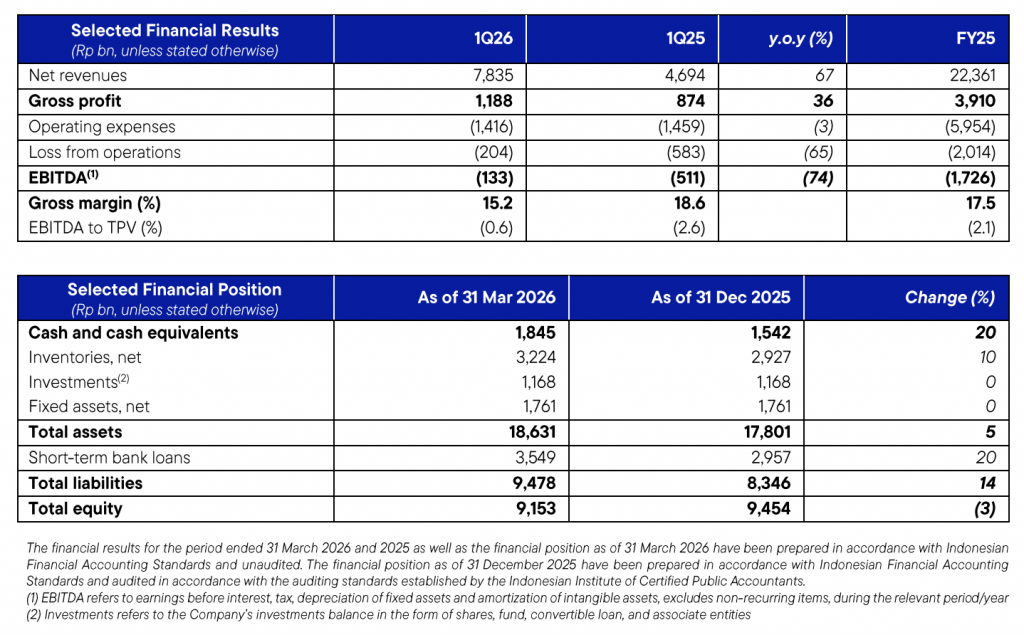

- Consolidated Net Revenues grew by 67% y.o.y from Rp4,694 bn in 1Q25 to Rp7,835 bn in 1Q26, contributed from improved performances in all segments, especially in the Institutions and Physical Stores on the back of higher smartphones sales.

- Take Rate expanded further from 9.0% in 1Q25 to 9.9% in 1Q26, on the back of Take Rate increase especially in 1P Retail and Institutions segments. This was a result of 21% y.o.y growth in Gross Profit Before Discount (GPBD) during the period.

- Better cost structure reflected by the lower consolidated Operating Expenses as percentage of TPV from 7.3% in 1Q25 to 6.4% in 1Q26, resulted in an improved performance of consolidated EBITDA as percentage of TPV of 200bps y.o.y.

- Ecosystem integration was further enhanced with the expanded feature of Blibli Affiliate into tiket.com platform, which is expected to further boost number of transacting users going forward.

- Having expanded its presence in the Physical Stores segment further by adding a total of 35 new stores in 1Q26, thus as at the end of March 2026, the Company operated a total of 295 consumer electronics stores, 9 home appliances electronics stores, and 1 fashion & sports store. In addition, the Company also managed 58 premium supermarkets outlets and 37 home and living experience centers.

MANAGEMENT STATEMENT(S)

Kusumo Martanto – CEO & Co-Founder

“We began the year 2026 with solid momentum, extending the positive trajectory from the previous quarter. Our first quarter results reflect continued execution of our strategy, delivering strong double-digit top line growth alongside further expansion in take rate and overall margins. At the same time, we successfully drove meaningful improvements in profitability performance, underscoring our focus on sustainable and disciplined execution.

Performance across our business remains well-balanced. Our core commerce segment continues to anchor growth, supported by strong demand in key categories and a more focused approach to higher-margin products. Our omnichannel playbook is scaling across categories, while our institutional and physical stores businesses are expanding with improved quality and scale.

We are also making steady progress in building a more integrated and scalable platform. Our integrated fulfillment service under FAS business is gaining traction as a key enabler of our omnichannel model, while ecosystem integration initiatives are driving higher engagement across platforms. In parallel, we are leveraging AI to enhance product discovery and customer decision-making, supporting higher conversion and platform productivity.

We remain on track to deliver our 2026 guidance. Our strengthened capabilities across talent, technology, and infrastructure—combined with seamless collaboration throughout our ecosystem—provide a solid foundation to execute our strategies with focus and discipline. The goal going forward is clear: scale our omnichannel capabilities, deepen ecosystem integration, and continue improving profitability performance as we drive long-term shareholder value.”

Ronald Winardi – CFO

“Throughout the first quarter, we managed to deliver strong revenue acceleration alongside continued progress in operating discipline and profitability. Net revenues grew robustly by 67% y.o.y, reflecting improved omnichannel monetization and solid ecosystem execution, while tighter cost control drove meaningful gains in efficiency. This translated into a significant narrowing of operating losses, resulted in a substantial improvement in our EBITDA performance to 0.6% as percentage of TPV, underscoring strengthening unit economics and operating leverage as we advance toward our profitability roadmap.”

KEY OPERATIONAL HIGHLIGHTS

BUSINESS SEGMENTS OVERVIEW

Below is an overview from each of the Company’s business segments during the first quarter of 2026 (1Q26) compared to the first quarter of 2025 (1Q25) period.

1P Retail

1P Retail segment undertakes the Company’s business through its B2C online commerce platform for first party (1P) products and services from various categories.

GPBD for this segment recorded a solid 23% y.o.y growth in 1Q26 to Rp564 bn. The improved GPBD performance was largely attributable to the Company’s selective growth strategy with the focus on higher-margin product categories, including new product launches in smartphones category, as well as faster growth trend in the home appliances electronics and lifestyle products. In addition, the Company’s home & living business also recorded improved performances on the back of improved productivity and higher economies of scale. As a result, Take Rate for this segment was successfully recorded as high as 24.8% in the 1Q26 period. Overall TPV and Net Revenues for this segment grew by 21% and 13% y.o.y in 1Q26 to Rp2,272 bn and Rp1,574 bn, respectively.

To support its 1P Retail segment, the Company has a vast network of order fulfillment, logistics and last-mile delivery infrastructure, using hub-and-spoke model, supported by 15 warehouses with a total warehouse area of approximately 200,000 square meters, as well as 19 distribution centers (hubs), enabling the Company to offer 2-hour delivery service of more than 400,000 SKUs in approximately 40 cities nationwide.

The warehouse in Marunda, West Java, serves as the main supply chain hub that strengthens the Company’s logistics and fulfillment capabilities, including Fulfillment at Speed (FAS) and Fulfillment by Blibli (FBB) services. Fulfillment business under FAS service has taken a leap step by deepening partnership to multiple Indonesia’s leading brand principals, further enhancing supply chain integration and accelerating order fulfillment efficiency.

As at the end of March 2026, the Company managed 37 home and living experience centers operated by Dekoruma, to expand consumer omnichannel touchpoints in the home & living category for this segment.

3P Retail

3P Retail segment predominantly records the Company’s platform revenue generated from sales of products and services of various categories from third party (3P) sellers through its online commerce and online travel agent (OTA) platforms.

GPBD for this segment recorded a 1% y.o.y growth in 1Q26 to Rp708 bn. The improved GPBD performance was mainly driven by price optimization and monetization expansion of ancillary revenues as well as overall operating efficiency measures implemented in the OTA business, amidst uncertainties due to global macro environment. Overall Net Revenues for this segment grew by 9% y.o.y in 1Q26 to Rp384 bn.

As at the end March 2026, the Company’s OTA platform – tiket.com offered a variety of products and services, including flight tickets from 143 domestic and international airlines serving more than 240 countries, regions, and territories, providing more than 3.6 million accommodation options, including more than 2.2 million options of alternative accommodations, and offering more than 103,400 activities and tourist destinations as well as more than 4,400 events worldwide.

Institutions

Institutions segment includes the Company’s commerce business through its online platforms for 1P and 3P products and services serving institutional clients across Indonesia.

GPBD for this segment recorded a strong 113% y.o.y growth in 1Q26 to Rp430 bn. The improved GPBD performance was mainly contributed to the success in regional expansion on the smartphones and home appliances electronics categories, which resulted in a higher sales volume to institution clients. During the period, this segment also managed to significantly improve the quality of its clients, reflected in higher spending per institutional client by 125% y.o.y to Rp112.0 mn. Overall TPV and Net Revenues for this segment grew by 77% and 137% y.o.y in 1Q26, to Rp4,906 bn and Rp3,553 bn, respectively.

Throughout the period, the Company’s Institutions segment served more than 43,800 institutional clients, with a continuous growth of monetization rate from 54% in 1Q25 to 72% in 1Q26, reflecting increasing trust by institutional clients on the services provided by the Company.

Physical Stores

Physical Stores segment records the Company’s business in physical consumer electronics stores (focusing on smartphones, tablets and related products), home appliances electronics stores, and fashion & sports stores, collaborating with leading global brand principals, as well as premium grocery supermarkets chain operated by subsidiary, PT Supra Boga Lestari Tbk (“Ranch Market”; IDX: RANC).

GPBD for this segment recorded a healthy 9% y.o.y growth in 1Q26 to Rp465 bn. The improved GPBD performance was mainly driven by the higher smartphone sales volume on the back of new products launch and the continued expansion of the Company’s consumer electronics stores. In addition, the Company’s supermarket outlets also recorded better margin during the period with improved Same-Store Sales Growth (SSSG) especially in the premium segment stores as well as better overall shrinkage management. Overall TPV and Net Revenues for this segment grew by 54% and 60% y.o.y in 1Q26, to Rp2,700 bn and Rp2,324 bn, respectively.

With the addition of 35 new stores throughout the period, the Company operated a total of 295 consumer electronics stores, which consisted of 151 monobrand stores and 144 multibrand stores, as well as 9 home appliances electronics stores and 1 fashion & sports store as at the end of March 2026. In addition, the Company also managed 58 premium supermarket outlets operated by Ranch Market.

CONSOLIDATED FINANCIAL PERFORMANCES

MANAGEMENT DISCUSSION & ANALYSIS

Below are brief descriptions of the Company’s consolidated financial performance during the first quarter of 2026 (1Q26) compared to the first quarter of 2025 (1Q25) period.

Revenue & Profitability

Consolidated Net Revenues recorded a solid 67% y.o.y growth from Rp4,694 bn in 1Q25 to Rp7,835 bn in 1Q26, driven by the improved contribution across all business segments, especially in the consumer electronics category, which benefited from higher smartphones sales volume, improved contribution from the OTA and institutional businesses, as well as an expanding physical stores network to support the Company’s omnichannel strategy. The changes in product mix resulted in a normalized overall consolidated Gross Margin to 15.2% in 1Q26.

Throughout the period, the Company managed to further improve its operational excellence which resulted in a better cost structure, reflected in lower consolidated Operating Expenses as percentage of TPV from 7.3% in 1Q25 to 6.4% in 1Q26, mainly supported by the lower consolidated advertising and marketing as well as general and administrative expenses as percentage of TPV. Overall, the Company continued to improve its performance, reflected by the improved consolidated EBITDA as percentage of TPV from -2.6% in 1Q25 to -0.6% in 1Q26, an improvement of 200bps y.o.y.

Cash Flows

Net cash used in operating activities was recorded at Rp109 bn in 1Q26, mainly due to investment in working capital to support accelerating Net Revenues growth. Net cash used in investing activities was recorded at Rp91 bn in 1Q26, mainly used for acquisition of fixed assets. Meanwhile, net cash provided by financing activities was recorded at Rp503 bn in 1Q26. Therefore, the Company’s consolidated Cash and Cash Equivalents position was recorded at Rp1,845 bn as of 31 March 2026 compared to Rp1,542 bn as of 31 December 2025.

Performance Guidance

The Company reiterates its target to achieve a 15–20% increase in consolidated Net Revenues in 2026. This target is supported by key strategic priorities to be executed for the remainder of the year, with a continued focus on margin improvement and a more efficient cost structure.

ENVIRONMENTAL, SOCIAL & GOVERNANCE (ESG)

The Company remains committed in delivering long-term value by actively driving positive impact. This includes taking tangible steps to manage environmental sustainability, empower employees and communities, and reinforce corporate governance practices to uphold transparency, accountability, and trust.

The Company continues to enhance its Environmental, Social and Governance (ESG) impact through the “Blibli Tiket Action”—an overarching program designed to integrate sustainability across operations within the ecosystem. Key initiatives implemented under this program include:

- Adoption of FSC-certified cardboard in order fulfillment to strengthen responsible sourcing practices.

- Optimization of the “Take-Back Packaging” program, enabling customers to return used packaging while supporting reforestation initiatives.

- Expansion of internal waste management through “CollaborAction” initiative, an employee education platform focused on increasing reuse and recycling rates across main offices within the ecosystem.

- Expansion of “Gadget for Good”, an e-waste management program, with five dropboxes deployed across Blibli Stores in the Greater Jakarta area to facilitate responsible waste disposal.

- Strengthening the “New Winning Values”, supported by ambassador assignments and ongoing engagement programs to enhance workforce readiness and cross-functional collaboration.

- Execution of corporate social responsibility (CSR) initiatives, encouraging employee and customer participation in donating pre-owned fashion items to beneficiaries in Bantar Gebang, East Jakarta.

- Enhancement of corporate governance through a strong focus on secure and reliable data management, in compliance with internationally recognized standards, including ISO 27001:2022, ISO 27701:2019, and PCI DSS 4.0.1.

- External recognition by Change the World award by Fortune Indonesia for the “Langkah Membumi” program, highlighting its impact on consumer sustainability education.

BUSINESS PROSPECTS

The Company expects to sustain its positive momentum into the remainder of 2026, supported by consistent execution of its omnichannel strategy and improving operating fundamentals. Amidst the macro challenges which impacting consumers spending power, the Company’s focus going forward remains on driving quality growth, enhancing margins, and continuing the path toward profitability, underpinned by a stronger product mix and disciplined cost management.

In parallel, the Company will continue to strengthen its ecosystem by scaling omnichannel capabilities, expanding fulfillment and service integration, and leveraging technology to enhance customer experience and engagement. These efforts position the Company to remain on track with its 2026 guidance while supporting sustainable growth and long-term value creation.

– End –