PT Global Digital Niaga Tbk (the “Company”; IDX: BELI), a pioneer and leading omnichannel commerce and lifestyle ecosystem in Indonesia focusing on serving digitally connected retail and institutions consumers, today announced its full year earnings results for the year 2025.

KEY HIGHLIGHTS

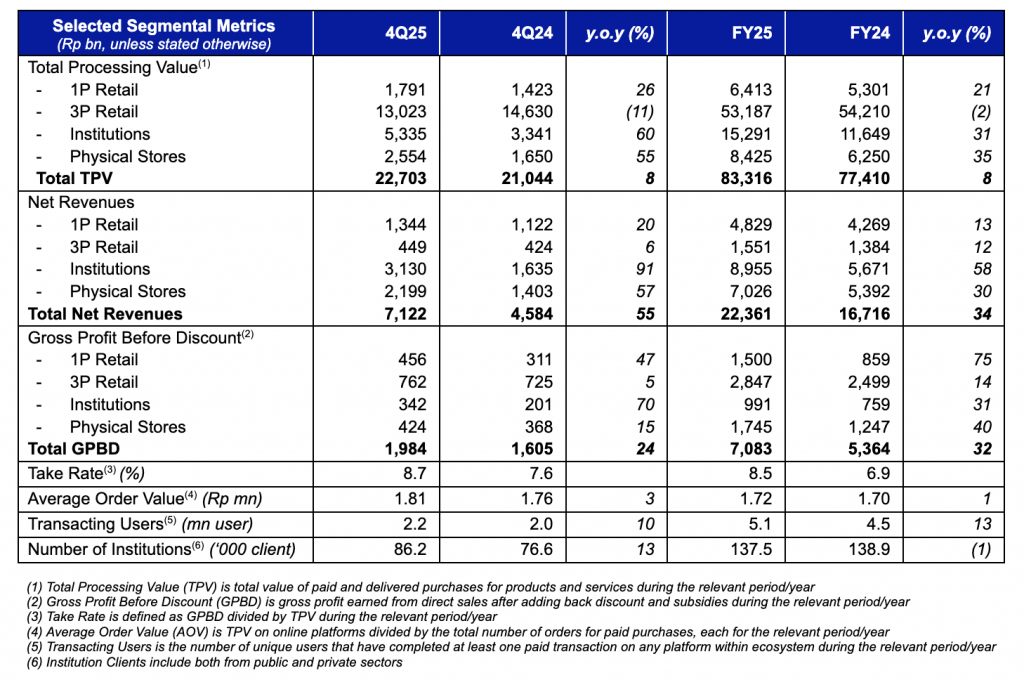

- Consolidated Net Revenues grew by 55% y.o.y in 4Q25 to Rp7,122 bn and by 34% y.o.y in FY25 to Rp22,361 bn, mainly contributed from higher smartphone omnichannel sales volume during the year.

- Take Rate expanded further from 6.9% in FY24 to 8.5% in FY25, reaching as high as 8.7% in 4Q25, on the back of Take Rate increase, especially in 1P Retail and Physical Stores segments. This was a result of 32% y.o.y growth in Gross Profit Before Discount (GPBD) during the year.

- Better cost structure reflected by the lower consolidated Operating Expenses as percentage of TPV from 7.4% in FY24 to 7.1% in FY25, resulted in an improved performance of consolidated EBITDA as percentage of TPV of 60bps y.o.y.

- Ecosystem integration has been advanced materially with the full roll-out of the Unified Membership and the Unified Loyalty Program across all platforms – Blibli, tiket.com, Ranch Market and Dekoruma.

- Having expanded its presence in the Physical Stores segment further by adding a total of 34 stores in 4Q25, as at the end of 2025 the Company operated a total of 265 consumer electronics stores, 4 home appliances electronics stores, and 1 fashion & sports store. In addition, the Company also managed 57 premium supermarkets outlets and 39 home and living experience centers.

MANAGEMENT STATEMENT(S)

Kusumo Martanto – CEO & Co-Founder

“The year 2025 marks a decisive step forward for the Company. In a year characterized by moderating household consumption in Indonesia, persistent pressure on consumer purchasing power, and intensifying competition across e-commerce, we stayed the course on what matters most: building a durable, integrated omnichannel ecosystem that creates value for customers, brand principals, and shareholders alike.

The results speak to the strength of that approach. We grew our revenues meaningfully whilst simultaneously improving our profitability trajectory — a combination that reflects the quality of our execution, not merely scale for its own sake. The deliberate shift towards higher-margin, competitively differentiated categories continued to pay off through take rate expansion, whilst the scaling of our omnichannel strategy was accretive to absolute gross profit before discount and overall ecosystem throughput. We are building a full-spectrum value chain across channels, and the resulting volume and density benefits strengthen our competitive position over time.

Our ecosystem integration advanced materially during the year. The full roll-out of Unified Membership and Blibli Tiket Rewards — now connecting Blibli, tiket.com, Ranch Market, and Dekoruma under a single engagement framework — deepens our relationship with customers across platforms and touchpoints. Dekoruma, in its first full year within the ecosystem, contributed meaningfully to the home & living category and broadened our omnichannel reach. These are not isolated initiatives; they are interconnected capabilities that compound as the ecosystem grows.

On the physical retail front, we expanded our consumer electronics and home appliances electronics stores network to 269 locations, up from 204 at end of previous year, across both monobrand and multibrand formats. This expansion deepened our penetration into tier-2 and tier-3 cities, strengthened last-mile distribution reach, and contributed to meaningful market share gains across our key brand partnerships. The physical network remains central to the end-to-end value proposition that positions the Company as a comprehensive omnichannel partner for brand principals.

We also continued to deepen deployment of data analytics, automation, and artificial intelligence across the enterprise, notable examples being merchandising, demand forecasting, and customer service operations. These are structural improvements to how we operate — they lower cost-per-order, sharpen decision-making, and scale with volume. Combined with ongoing cost discipline across the organization, they underpin the sustained improvement in our operating efficiency.

2026 will continue be a challenging year. Indonesian private consumption growth has moderated, consumers remain selective, and competitive intensity in e-commerce shows no sign of abating. We are not immune to these pressures. But we believe our integrated omnichannel model — which meets consumers online, in-store, and across hybrid journeys — is particularly well suited to navigate this landscape and to capture value as the market evolves.”

Ronald Winardi – CFO

“We delivered strong top-line performance during the year with growing 34% y.o.y net revenues, supported by broad-based segment improvements, particularly in consumer electronics and the continued expansion of our omnichannel ecosystem. Further, our improved operational efficiency is reflected in a leaner cost structure and a 60bps enhancement in EBITDA performance. Driven by sustained performance, ongoing initiatives, and a stronger cost and margin profile, we’re aiming for 15–20% net revenues growth in 2026.”

KEY OPERATIONAL HIGHLIGHTS

BUSINESS SEGMENTS OVERVIEW

Below is an overview from each of the Company’s business segments during the fourth quarter of 2025 (4Q25) compared to the fourth quarter of 2024 (4Q24) period, and the full year of 2025 (FY25) compared to the full year of 2024 (FY24).

1P Retail

1P Retail segment undertakes the Company’s business through its B2C online commerce platform for first party (1P) products and services from various categories.

GPBD for this segment recorded a solid 47% y.o.y growth in 4Q25 to Rp456 bn, and 75% y.o.y growth in FY25 to Rp1,500 bn. The improved GPBD performance was largely attributable to the Company’s strategic prioritization of higher-margin product categories, including new product launches in smartphones category, as well as benefiting from higher sports & lifestyle products offering. In addition, the Company’s home & living business recorded improved performances on the back of optimized product mix and higher margin products offering, including cross-sell. As a result, Take Rate for this segment was successfully recorded as high as 25.5% in the 4Q25 period. Overall TPV and Net Revenues for this segment grew by 21% and 13% y.o.y in FY25 to Rp6,413 bn and Rp4,829 bn, respectively.

To support its 1P Retail segment, the Company has a vast network of order fulfillment, logistics and last-mile delivery infrastructure, using hub-and-spoke model, supported by 13 warehouses with a total warehouse area of approximately 200,000 square meters, as well as 19 distribution centers (hubs), enabling the Company to offer 2-hour delivery service of more than 400,000 SKUs in more than 40 cities nationwide.

The warehouse in Marunda, West Java, serves as the main supply chain hub that strengthens the Company’s logistics and fulfillment capabilities, including Fulfillment at Speed (FAS) and Fulfillment by Blibli (FBB) services. Fulfillment business under FAS service has taken a leap step by deepening partnership to multiple Indonesia’s leading brand principals, further enhancing supply chain integration and accelerating order fulfillment efficiency.

As at the end of 2025, the Company manages 39 home and living experience centers operated by Dekoruma, to expand consumer omnichannel touchpoints in the home & living category for this segment.

3P Retail

3P Retail segment predominantly records the Company’s platform revenue generated from sales of products and services of various categories from third party (3P) sellers through its online commerce and online travel agent (OTA) platforms.

GPBD for this segment recorded a 5% y.o.y growth in 4Q25 to Rp762 bn, and 14% y.o.y growth in FY25 to Rp2,847 bn. The improved GPBD performance was mainly driven by significant focus shift on the OTA business into higher margin products category, including accommodation and experiences, as well as overall operating efficiency measures implemented. Overall Net Revenues for this segment grew by 12% y.o.y in FY25 to Rp1,551 bn.

As at the end 2025, the Company’s OTA platform – tiket.com offered a variety of products and services, including flight tickets from 143 domestic and international airlines serving more than 240 countries, regions, and territories, providing more than 3.6 million accommodation options, including more than 2.2 million options of alternative accommodations, and offering more than 77,700 activities and tourist destinations as well as more than 4,300 events worldwide.

Institutions

Institutions segment includes the Company’s commerce business through its online platforms for 1P and 3P products and services serving institutional clients across Indonesia.

GPBD for this segment recorded a strong 70% y.o.y growth in 4Q25 to Rp342 bn, and 31% y.o.y growth in FY25 to Rp991 bn. The improved GPBD performance was mainly contributed to the success in regional expansion which resulted in a higher sales volume to institution clients. In FY25, this segment also managed to improve further the quality of its clients, reflected in higher spending per institutional client by 33% y.o.y to Rp111.2 mn. Overall TPV and Net Revenues for this segment grew by 31% and 58% y.o.y in FY25, to Rp15,291 bn and Rp8,955 bn, respectively.

Throughout 2025, the Company’s Institutions segment served more than 137,500 institutional clients, with a continuous growth of monetization rate from 49% in FY24 to 59% in FY25, reflecting increasing trust by institutional clients on the services provided by the Company.

Physical Stores

Physical Stores segment records the Company’s business in physical consumer electronics stores (focusing on smartphones, tablets and related products), home appliances electronics stores, and fashion & sports stores, collaborating with leading global brand principals, as well as premium grocery supermarkets chain operated by subsidiary, PT Supra Boga Lestari Tbk (“Ranch Market”; IDX: RANC).

GPBD for this segment recorded a healthy 15% y.o.y growth in 4Q25 to Rp424 bn, and 40% y.o.y growth in FY25 to Rp1,745 bn. The improved GPBD performance was mainly driven by the higher smartphone sales volume on the back of new products launch and the continued expansion of the Company’s consumer electronics stores. In addition, the Company’s supermarket outlets also recorded better margin during the year with improved Same-Store Sales Growth (SSSG) and better shrinkage management. Overall TPV and Net Revenues for this segment grew by 35% and 30% y.o.y in FY25, to Rp8,425 bn and Rp7,026 bn, respectively.

With the addition of 61 new consumer electronics stores throughout 2025, wherein 29 new stores were added during the fourth quarter, the Company operated a total of 265 consumer electronics stores as at the end of 2025, which consisted of 141 monobrand stores and 124 multibrand stores. In addition, the Company also managed 57 premium supermarket outlets operated by Ranch Market. During the fourth quarter, the Company also rolled out the opening of new 4 home appliances electronics stores (called “Blibli Elektronik”) and 1 fashion & sports store (called “BlibliStyle Outlet”), to enhance its omnichannel strategy in these categories.

CONSOLIDATED FINANCIAL PERFORMANCES

MANAGEMENT DISCUSSION & ANALYSIS

Below are brief descriptions of the Company’s consolidated financial performance during the fourth quarter of 2025 (4Q25) compared to the fourth quarter of 2024 (4Q24) period, and the full year of 2025 (FY25) compared to the full year of 2024 (FY24).

Revenue & Profitability

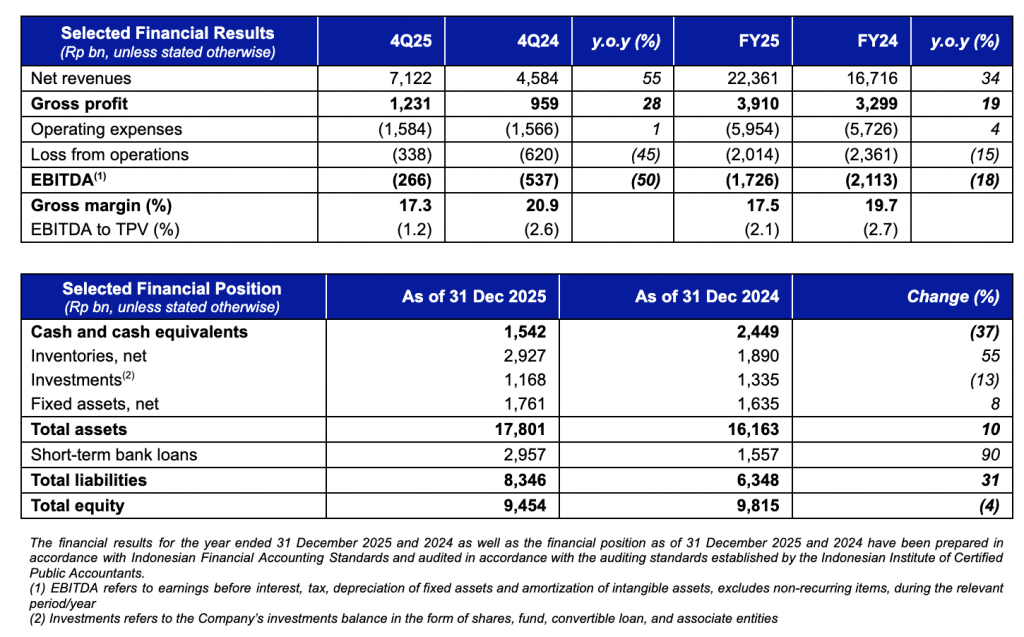

Consolidated Net Revenues recorded a solid 55% y.o.y growth from Rp4,584 bn in 4Q24 to Rp7,122 bn in 4Q25, and 34% y.o.y growth from Rp16,716 bn in FY24 to Rp22,361 bn in FY25, driven by the improvement across all business segments, especially in the consumer electronics category, which benefited from higher smartphones sales volume, improved contribution from the Company’s institutional business, and an expanding physical stores network to support the Company’s omnichannel strategy. However, the changes in product mix resulted in a slight decline in overall consolidated Gross Margin to 17.5% in FY25.

Throughout the year, the Company managed to further improve its operational excellence which resulted in a better cost structure, reflected in lower consolidated Operating Expenses as percentage of TPV from 7.4% in FY24 to 7.1% in FY25, mainly supported by the lower consolidated advertising and marketing as well as general and administrative expenses as percentage of TPV. Overall, the Company continued to improve its performance, reflected by the improved consolidated EBITDA as percentage of TPV from -2.7% in FY24 to -2.1% in FY25, an improvement of 60bps y.o.y.

Cash Flows

Net cash used in operating activities was recorded at Rp3,520 bn in FY25, mainly due to investment in working capital to support accelerating Net Revenues growth. Net cash used in investing activities was recorded at Rp390 bn in FY25, mainly used for acquisition of fixed assets. Meanwhile, net cash provided by financing activities was recorded at Rp3,003 bn in FY25. Therefore, the Company’s consolidated Cash and Cash Equivalents position was recorded at Rp1,542 bn as of 31 December 2025 compared to Rp2,449 bn as of 31 December 2024.

Performance Guidance

Considering historical revenue growth trends and the initiatives undertaken throughout the year, the Company is targeting a 15–20% increase in consolidated Net Revenues in 2026. This target is supported by key strategic priorities to be executed in the coming year, with a continued focus on margin improvement and a more efficient cost structure.

ENVIRONMENTAL, SOCIAL & GOVERNANCE (ESG)

The Company remains committed in creating long-term value through sustainable practices, reflected in the Blibli Tiket Action program that advances ESG initiatives and fosters active stakeholders engagement throughout 2025:

Environmental Focus

Strengthened its environmental impact through customer and employee-driven initiatives.

- Take-Back Packaging Program: approximately 14,500 packages collected, driving circularity and one tree planted per 10 returns.

- Green Delivery: reduced carbon emissions through electric vehicle usage, with over 59,000 transactions throughout the year.

- Trade-In Expansion: included lifestyle items, extending the life of products and minimizing waste.

- Misi Tanam Pohon Program: enabled customers to contribute to tree planting through transactions, resulting in 16,000 mangrove trees planted in 2025, bringing the total to 31,000 trees since 2021.

- Langkah Membumi Ecoground: a 4th-year sustainability movement driving eco-conscious lifestyles through sport and community engagement, featuring 44 educational sessions and delivering measurable impact: 94+ tCO₂e reduced, with 16,000 trees planted, and 100% waste managed.

- Tiket Green: enabled responsible travel choices with 370,000+ eco-friendly accommodations worldwide, including 19,000+ across Indonesia and Southeast Asia.

- Kaizen Competition: Fostered a culture of continuous improvement and operational efficiency.

- One Step Further Program: Promoted circular fashion through employee-led donations of gently used shoes to Desa Mendut, Magelang, Central Java.

Social Impact

Driving inclusive growth through education, empowerment, and capability building.

- Educational Empowerment: through the BUBBLE Program in collaboration with Rumah Belajar, provided learning support for children with limited access to education in West Jakarta. Additionally, Blizania Roleplay Activity introduced children from Yayasan Sanggar Anak Kita (SAKA) to the digital world and e-commerce through interactive play.

- Foster Inclusivity: partnered with Sandiaga Uno and YAMSA to inspire youth through the “Jumbo” film screening, and with Yayasan Tunas Mulia to donate used clothes to families in Bantargebang area.

- Jagoan Pariwisata: empowered MSMEs by capacity building through employee-led mentorship program, funding support, enabling seamless onboarding onto Blibli and tiket.com platforms.

- BOLD Learning Festival: featured 19+ speakers across 19 learning sessions, enhancing employee capabilities through interactive learning on professional and personal development.

- CollaborAction: engaged 100 employees across functions and entities to strengthen understanding and application of sustainability practices in daily operations.

- Reinforced Core Culture Principle: fostered an inclusive and collaborative culture through the launch of Winning Principle—Customer First, Act Fast & Practical, Be the Solution, and Continuous Improvement.

- Disability Internship Program with Yayasan Helping Hands: provided structured internships, mentoring, and tailored workplace support to enhance participants’ job readiness, independence, and confidence.

Governance Excellence

Continued to show strong commitment to uphold good corporate governance practice:

- Data Security & Privacy: maintained PCI DSS 4.0 Merchant Level 1, ISO/IEC 27001:2022, and ISO/IEC 27701:2019 certifications, reinforcing commitment to data security, privacy, and responsible digital governance.

- Awards & Recognition: ranked #72 on the list of Fortune Indonesia 100, ranked #260 on the list of Fortune Southeast Asia 500, recognized for strong governance and sustainability with the award SWA Most Reputable Company Champion (Excellence), ASRRAT Gold 2025, and Fortune Change the World Award 2025 for Jagoan Pariwisata.

BUSINESS PROSPECTS

The Company expects the operating environment in 2026 to remain challenging, with consumer sentiment likely to recover gradually amid global macroeconomic uncertainty and continued competitive intensity in e-commerce. Against this backdrop, the Company will focus on three strategic priorities.

First, the Company will continue to sharpen its path to profitability by further improving category mix, expanding partnerships with brand principals, and reducing fulfillment cost-per-order through network optimization and automation. The Company targets continued improvement in EBITDA performance in the upcoming year.

Second, the Company will deepen ecosystem monetization. Unified Membership and Blibli Tiket Rewards will be enhanced with personalized engagement capabilities, and the Company will pursue incremental revenue streams from differentiated ancillary revenues and value-added fulfillment offerings for brand principals and third-party sellers.

Third, the Company will invest selectively in physical retail expansion and omnichannel infrastructure, focusing on formats and locations that deliver attractive unit economics and strengthen competitive differentiation in categories where offline experience drives conversion — including consumer electronics, home appliances electronics and home & living.

With Indonesia’s long-term consumption growth trajectory intact, a young and digitally engaged population, an increasingly integrated ecosystem that is a deep and unique moat, the Company is well positioned to convert operational improvements into sustainable value creation for all stakeholders.

-END-