31st July 2024 | Jakarta, Indonesia

PT Global Digital Niaga Tbk (the “Company”; IDX: BELI), a pioneer and leading omnichannel commerce and lifestyle ecosystem in Indonesia focusing on serving digitally connected retail and institutions consumers, today announced its second quarter earnings results for the year 2024.

KEY HIGHLIGHTS

- Consolidated Net Revenues slightly grew by 1% y.o.y in 1H24. The Company’s growth focus remains selective in relatively higher margin categories, faster turnover and strategic positioning enhancement.

- Take Rate continued to expand from 4.8% in 1H23 to 6.5% in 1H24, resulting in 33% y.o.y growth in Gross Profit Before Discount (“GPBD”). Consolidated Gross Margin also continued to improve from 15.3% in 1H23 to 19.7% in 1H24, an increase of 440-bps y.o.y, mainly contributed by the Gross Margin expansion in most of the business segments.

- Cost structure continued to improve further, reflected by the lower consolidated Operating Expenses as percentage of TPV from 7.9% in 1H23 to 7.5% in 1H24, resulted in an improved performance of consolidated EBITDA as percentage of TPV by 140-bps y.o.y, from -4.3% in 1H23 to -2.9% in 1H24.

- As a testament of the Company’s commitment in enhancing users’ experience across platform, launched a Unified Membership feature which provides the benefits of a seamless access and unified login experience for all users in Blibli Tiket ecosystem.

- The construction progress of the new warehouse in Marunda was almost completed as at the end of June 2024 and is in line with the target to start operation in October this year.

- Completed the purchase of approximately 99.83% of share ownership in PT Dekoruma Inovasi Lestari (“Dekoruma”) to broaden the scope of the home and living products category as another key vertical to strengthen the Company’s omnichannel strategy.

- With the additional of 13 consumer electronic stores throughout the second quarter of 2024, the Company operated a total of 185 consumer electronics stores, as well as 62 premium supermarkets outlets and 30 home and living experience centers as at the end of June 2024.

- Carried out Annual General Meeting of Shareholders (“AGMS”) and Extraordinary General Meeting of Shareholders (“EGMS”), where all the agendas’ items proposed were approved.

MANAGEMENT STATEMENT(S)

Kusumo Martanto – CEO & Co-Founder

“We began this year navigating through a period of economic headwinds and demand variability preceding the election, yet I am pleased to report that the Company has demonstrated remarkable resilience and margin growth throughout the first half of the year which are in line with the Company’s focus towards profitability. This steadfast performance underscores the strength of our business model and the solid foundation we have built for sustained success.

Our relentless focus on customer satisfaction continues to be the cornerstone of our strategy, driving innovation and synergy across our omnichannel ecosystem. The introduction of our Unified Membership feature is a testament to our commitment to enhance user experience across platforms. Moreover, the integration of cutting-edge Artificial Intelligence capabilities, such as LLM and GenAI, has been transformative. These technologies have significantly improved our product, category, and promotion recommendations by leveraging user behavior, product performance, and characteristics, nearly doubling our click-through rates.

Our omnichannel strategy is further bolstered by the expansion of physical consumer electronics stores nationwide, in partnership with leading global brands. Additionally, our strategic acquisition of Dekoruma marks a pivotal step forward in expanding our omnichannel portfolio into the home and living products category. These initiatives are designed to create a seamless and sustainable omnichannel experience for our customers, effectively and seamlessly bridging the online and offline realms, while further strengthening our position as the omnichannel leader in Indonesia.

I would also like to extend my heartfelt gratitude to our shareholders for their unwavering support during the GMS last June. Your confidence and belief in our vision have been instrumental in our journey, motivating us to grow stronger and strive for greater heights. We remain committed in driving long-term value and are confident that our strategic initiatives will continue to deliver robust growth and profitability. Thank you for your continued trust and support.”

Ronald Winardi – CFO

“Selective Omnichannel growth strategy, rigorous pursuit of gross profit expansion and discipline cost control have been effective in improving our consolidated EBITDA losses by 38% y.o.y in 2Q24.”

KEY OPERATIONAL HIGHLIGHTS

SEGMENTAL OVERVIEW

Below is an overview from each of the Company’s business segments during the second quarter of 2024 (2Q24) compared to the second quarter of 2023 (2Q23) period, and the first half of 2024 (1H24) compared to the first half of 2023 (1H23) period.

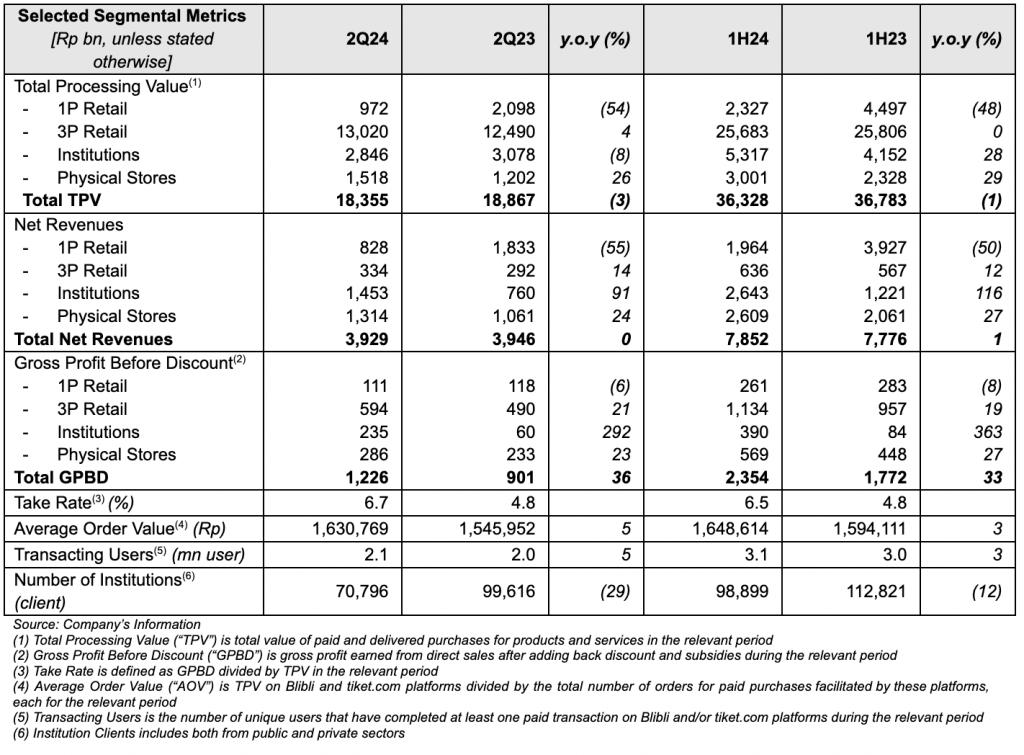

1P Retail

1P Retail segment undertakes the Company’s business through its B2C online commerce platform for first-party (1P) products and services from various categories.

GPBD for this segment experienced a slight decline by 6% y.o.y from Rp118 bn in 2Q23 to Rp111 bn in 2Q24, and by 8% y.o.y from Rp283 bn in 1H23 to Rp261 bn in 1H24. The lower GPBD performance was mainly due to the decline in TPV and Net Revenues for this segment in both 2Q24 and 1H24 y.o.y as the Company still optimized its TPV mix throughout this period. Nevertheless, the rationalization has improved the Take Rate for this segment significantly during the period.

The construction progress of the Company’s new warehouse in Marunda, West Java, was almost completed, reached ~98% as at the end of June 2024 and is in line to start operation in October this year. The Marunda warehouse is built on 100,000-sqm land and is prepared to support the Company’s commitment to develop smart logistics and supply chain management.

3P Retail

3P Retail segment predominantly records the Company’s platform fees generated from sales of products and services of various categories from third-party (3P) sellers through its online commerce and online travel agent (“OTA”) platforms.

GPBD for this segment grew healthily by 21% y.o.y from Rp490 bn in 2Q23 to Rp594 bn in 2Q24, and by 19% from Rp957 bn in 1H23 to Rp1,134 bn in 1H24. The improved GPBD performance was mainly driven by higher margin from the B2C business on the back of an increase in published rate for its third-party sellers since the beginning of the year, as well as from robust travel demand on our OTA business. Overall Net Revenues for this segment grew by 14% y.o.y to Rp334 bn in 2Q24 and by 12% y.o.y to Rp636bn in 1H24.

As at the end of June 2024, the Company’s OTA platform – tiket.com, had a vast product assortment offering, including 116 airline partners covering 225 countries, regions, and territories, and more than 3.6 million accommodation listings, including 2.2 million alternative accommodations.

Institutions

Institutions segment includes the Company’s business through its B2B and B2G platforms for 1P and 3P products and services serving private and public-sector institutions across Indonesia.

GPBD for this segment continued to record significant growth by 292% y.o.y from Rp60 bn in 2Q23 to Rp235 bn in 2Q24, and by 363% y.o.y from Rp84 bn in 1H23 to Rp390 bn in 1H24. Throughout the period, this segment also managed to improve further the quality of its institutional clients, reflected by higher spending per institutional client by 46% y.o.y to Rp53.8 mn per client in 1H24, resulted in higher TPV and Net Revenues during the period by 28% and 116% y.o.y, respectively.

As at the end of June 2024, the Company’s Institutional segment has managed to serve and fulfill orders from more than 98,000 institutional clients. The monetization rate for this segment has also improved, reflected by higher Net Revenues as percentage of TPV from 29% in 1H23 to 50% in 1H24, reflecting continuous trusts from the institution clients towards the Company’s platforms to fulfil their corporate needs.

Physical Stores

Physical Stores segment records the Company’s business in physical consumer electronics stores collaborating with leading global consumer electronics brand principals, as well as premium grocery supermarkets chain operated by 70.6%-owned Subsidiary, PT Supra Boga Lestari Tbk (“Ranch Market”; IDX: RANC) and home and living experience centers network operated by Subsidiary, PT Dekoruma Inovasi Lestari (“Dekoruma”).

GPBD for this segment grew strongly by 23% y.o.y from Rp233 bn in 2Q23 to Rp286 bn in 2Q24, and by 27% y.o.y from Rp448 bn in 1H23 to Rp569 bn in 1H24. The improved GPBD performance was mainly driven by the increase in TPV and Net Revenues during the period as the Company continued to enjoy good run of sales volume growth for its smartphone and other IoT’s accessories aligned with the Company’s continuous expansion of its consumer electronic stores network nationwide. This positive trend reflects the Company’s success in rolling out its omnichannel strategy to provide seamless customer shopping experiences both online and offline.

With the additional of 13 new consumer electronics stores during the second quarter, the Company operated a total of 185 consumer electronics stores as at the end of June 2024, which consists of 98 monobrand stores (including 72 Samsung Stores and 15 hello stores, along with the other global leading brand stores), and 87 multibrand stores (including 60 Blibli Stores and 27 Tukar Tambah stores). In addition, the Company also managed 62 premium supermarket outlets operated by Ranch Market and 30 home and living experience centers operated by Dekoruma, to expand consumer omnichannel touchpoints nationwide.

CONSOLIDATED FINANCIAL PERFORMANCES

MANAGEMENT DISCUSSION & ANALYSIS

Below are brief descriptions of the Company’s consolidated financial performances during the second quarter of 2024 (2Q24) compared to the second quarter of 2023 (2Q23) period, and the first half of 2024 (1H24) compared to the first half of 2023 (1H23) period.

Revenue & Profitability

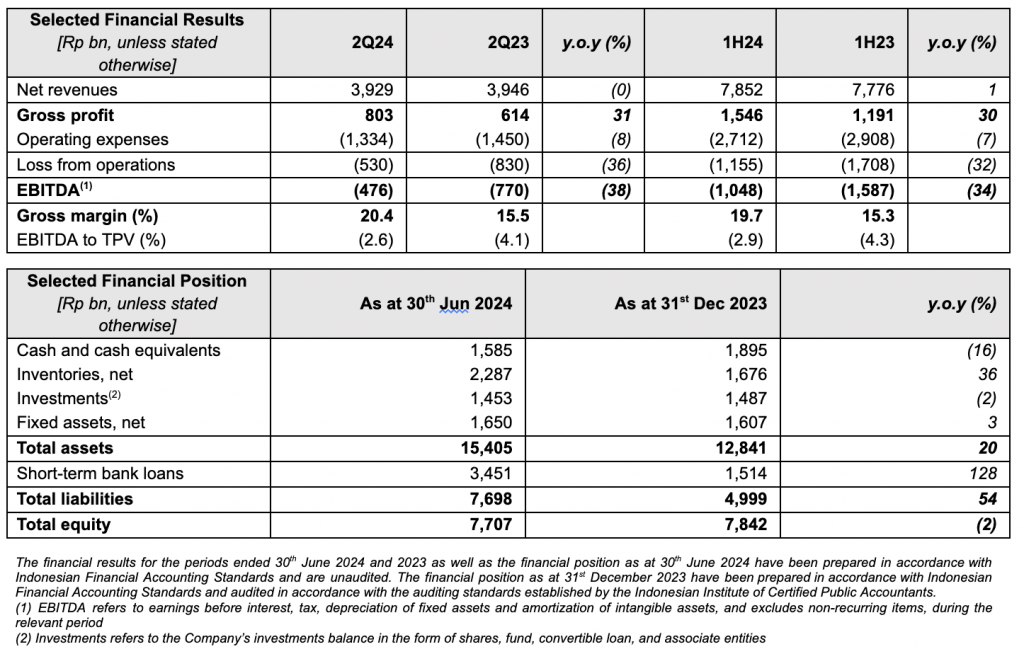

Consolidated Net Revenues recorded 1% y.o.y increase from Rp7,776 bn in 1H23 to Rp7,852 bn in 1H24, mainly driven by strong performance in the consumer electronics category on the back of higher smartphone sales volume, higher contribution from OTA business, as well as higher contribution from the Physical Stores segment supported by continuous expansion of consumer electronics stores network, partly offset by the optimization of product mix across categories in the 1P Retail segment. Despite the modest growth of consolidated Net Revenues during the period, the Company managed to continue improving its consolidated Gross Margin from 15.3% in 1H23 to 19.7% in 1H24, an improvement of 440-bps y.o.y, which was mainly contributed by the Gross Margin expansion in most of the business segments.

Throughout the period, the Company has successfully managed to further improve its operational excellence which resulted in better cost structure, reflected from lower consolidated Operating Expenses as percentage of TPV from 7.9% in 1H23 to 7.5% in 1H24, mainly supported by the lower advertising & marketing expenses as percentage of TPV in 1H24 y.o.y to 0.9%, and stable general and administrative expenses as percentage of TPV in 1H24 y.o.y at 5.0%, despite the additional of store rental and employee’s costs due to physical consumers electronics stores expansion.

With the improvement of consolidated Gross Margin and overall better cost structure, the Company continued to improve its loss performance, reflected by the lower consolidated EBITDA as percentage of TPV from -4.3% in 1H23 to -2.9% in 1H24, an improvement of 140-bps y.o.y.

Sustained Operating Cash Flows

Net cash used in operating activities was Rp2,016 bn in 1H24, slightly improved from Rp2,324 bn in 1H23. Meanwhile, the increase of net cash used in investing activities was mainly driven by the completion of purchase transaction of Dekoruma in June 2024. Improving margin, lower operating expenses and better working capital management contributed to a sustained operating cash flow, leading to the Company’s cash and cash equivalents position to Rp1,585 bn as at 30th June 2024.

CORPORATE ACTION(S)

On June 13th, 2024, the Company successfully held an AGMS for the financial year 2023, which was then followed by an EGMS in Jakarta.

During the AGMS, the Company’s shareholders approved and ratified the Board of Directors’ Report on the Company’s Annual Report for the financial year 2023, and other agendas including related to the determination of salary and other benefits of the Board of Directors and determination of honorarium and/or other benefits of the Board of Commissioners for the financial year 2024, appointment of Public Accountant and/or Public Accountant Firm to audit the Company’s financial statements ends on December 31st, 2024, and appointment of Mr. Suryadi Sasmita as the new Independent Commissioner. The Company also conveyed a report regarding the realization of the use of proceeds from the Company’s initial public offering up to December 31st, 2023.

Meanwhile, during the EGMS, the Company’s independent shareholders approved the Company’s plan to increase capital without pre-emptive rights (Penambahan Modal Tanpa Hak Memesan Efek Terlebih Dahulu (”PMTHMETD”)) through new share issuance with a maximum of 7.63% of the Company’s issued and paid-up capital, consisting of:

- issuance of new shares in the framework of the Company’s management and employee stock option plan (“MESOP Program”) with a maximum amount of 3.65% of the Company’s issued and paid-up capital; and

- issuance of new shares without pre-emptive rights other than in the framework of MESOP Program (“Capital Increase Other Than MESOP Program”) with a maximum amount of 3.98% of the Company’s issued and paid-up capital.

On Jun 21st, 2024, the Company also completed the purchase of 99.83% of all issued and fully paid shares in Dekoruma, a leading home and living omnichannel retail and interior design company in Indonesia. Post this transaction, together with Dekoruma, home and living category will be an additional pillar of growth tapping to burgeoning demand of well-designed and affordable home and living products for middle income segment.

ENVIRONMENTAL, SOCIAL AND GOVERNANCE (ESG)

As a pioneer of an integrated omnichannel commerce and lifestyle ecosystem, the Company’s commitment towards sustainability is further enhanced by introducing “Blibli Tiket Action”, an umbrella program supporting sustainability across ESG aspects by encouraging action and active involvement from all stakeholders to create a transformative impact and realize the program’s mission of making real impact through sustainable practices.

Throughout 1H24 period, Blibli Tiket Action has carried out several initiatives, including:

- Pioneered green delivery, by providing customers with a new shipping option using electric vehicles for the Company’s instant delivery service;

- In collaboration with EcoTouch, managed corporate waste by recycling fabric waste into new sustainable fabrics;

- Promoted continuous improvement efforts (kaizen) to enhance productivity and efficiency;

- Launched the “CollaborAction” program to enhance employees’ awareness and understanding of sustainability; and

- Initiated a Corporate Social Responsibilities (“CSR”) program during the last Ramadhan for employees to participate in sustainable initiatives such as fundraising, product donations, and volunteering efforts.

The company has successfully maintained its ISO/IEC 27001:2013 certification for the information security management system and has extended this certification to include its B2G and seller data systems, further enhancing data security.

In addition, the Company has been awarded the Best Execution Winner in the E-Commerce Industry and Outstanding Achievement in Sustainability and Governance for the Sustainability theme in the SPEx2® Award. These awards and recognition reflect the Company’s actions to create greater impacts toward sustainable practices.

BUSINESS PROSPECTS

Looking ahead, the Company is poised to further innovate and harness potential synergies within its ecosystem. Additionally, the Company will continue to execute its omnichannel strategy, which involves expanding consumer touchpoints by partnering with global leading brand principals. The aim is to offer a seamless customer experience and journey, regardless of the platform they access within the ecosystem. These strategic initiatives are expected to drive the growth of the business and maintain the favorable trajectory towards profitability. The Company remains committed to leverage its strengths and exploring new opportunities in delivering sustainable value for all its stakeholders.